Is inflation eating into your savings?

Have you ever heard someone say that “your savings are safe in the bank” or “you can’t lose money if you put it in a savings account”? There’s a lot of truth in this, but it does miss one point that means your savings aren’t quite as safe as you think.

The culprit is inflation. And if you’re leaving money in a bank account for the long term, or in any other form of ‘cash’ savings, it means you might be losing money without ever noticing it.

What is inflation?

Inflation describes the way that goods and services tend to rise in price over the years. The rate of inflation is how much they rise.

Sometimes the rate of inflation is high and the effects can be seen over the course of a year or two. When it’s low, the impact is less noticeable, but the effects still add up over the long term.

Purchasing power looks at how much your money will buy you. If you’ve ever found yourself saying that it’s costing you more money to buy the same things in the shops – or that you get less when you spend your usual amount – that’s an example of diminishing power.

Exploring the impact

If your money is in a bank account for a year or two, you won’t really notice the effects of inflation unless it’s very high. But let’s say you decide to leave your money in an interest-paying bank account for a decade, rather than investing it in the stock market.

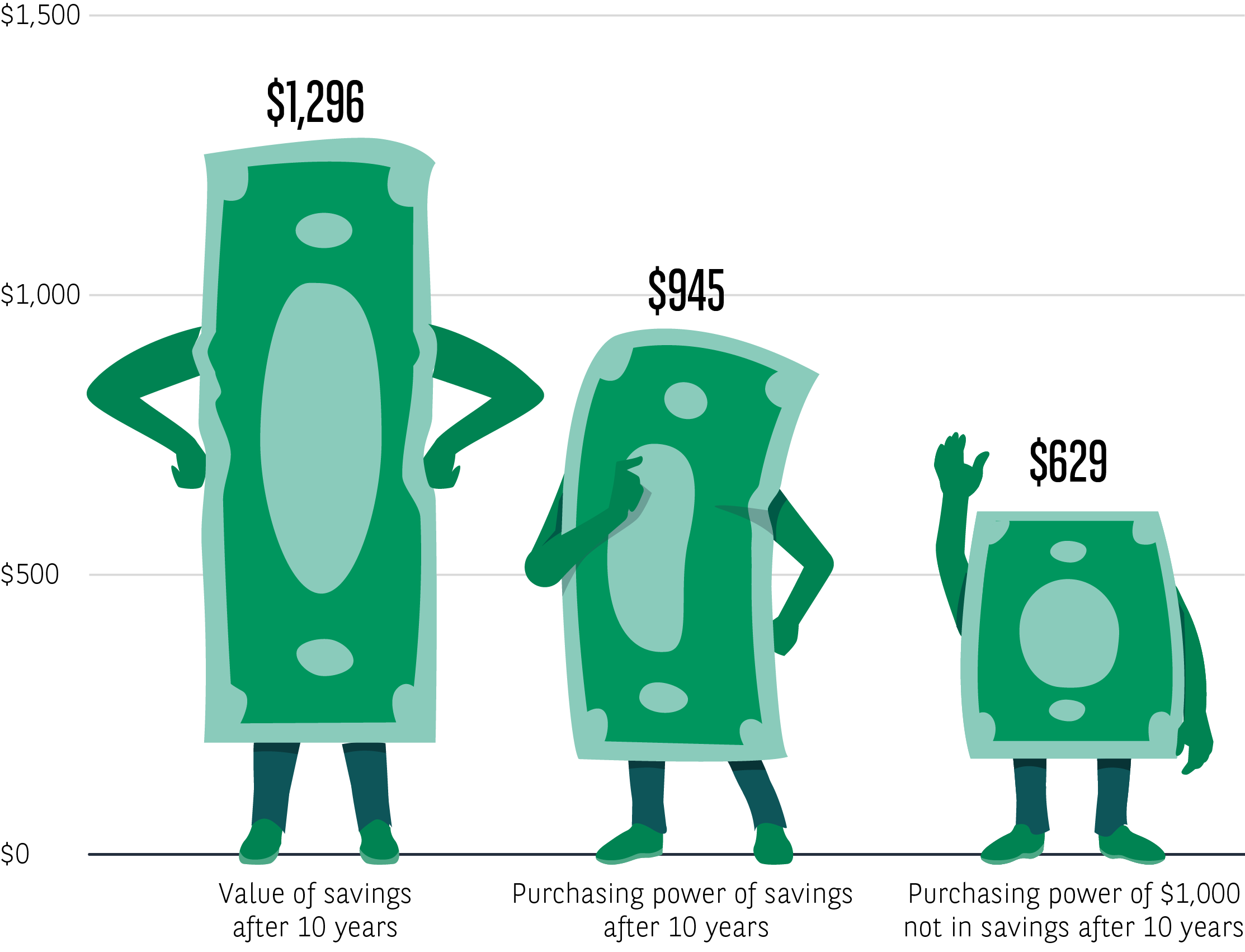

If you check it occasionally, you’ll probably see the amount in there is a little higher each time. It looks like you’re consistently making money, but let’s add inflation into the mix. Here’s an example based on $1,000 in a US savings account. This means we’ll be using US inflation and interest rates, but the broad idea applies to most countries around the world.

Growth of $1,000 in a US savings account vs. impact of inflation over 10 years

Source: Bloomberg, BNP Paribas Asset Management. Data from 31 December 2015 to 31 December 2025, US dollars. Rebased to 1000 as at graph start date.

You might think you’re safely making money year on year by earning interest, but that growth is actually being eaten away by inflation. After 10 years, it looks like you’ve made $1,296. However, when accounting for inflation, your purchasing power is in fact less than the $1,000 you started with. Of course, doing nothing with your money would mean it loses more than $370 in value!

Beating inflation

So, how do you beat inflation? The simple answer is that you need to produce higher returns than the rate of inflation. Ideally, quite a bit higher. Of course, that’s easy to say, but there are ways you can try to do it. One option is to step off the sidelines and explore the opportunities offered by the investment world.

If you do this, you do have to understand that investments don’t come with any guarantees and they can fall in value as well as rise. You may even find you get back less than you invest. However, they also offer the potential for significantly higher returns over the long term, as we explore in the other articles of the Don't sit on your cash series.

Don’t sit on your cash

Download our guide for information on stepping off the sidelines and into the investment world

Download the guide

More articles from our Don't sit on your cash mini-series