Avoiding locking in your losses

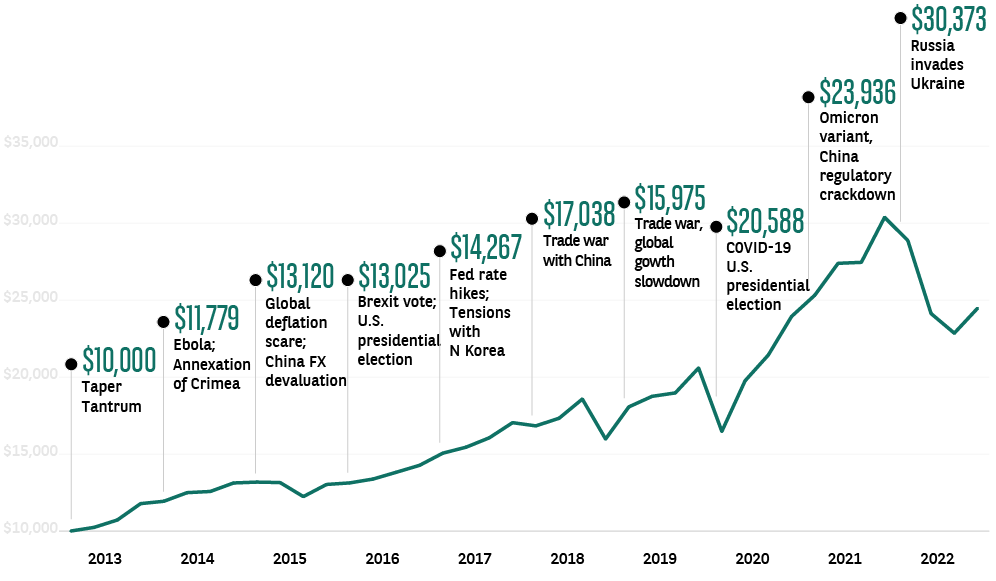

All investors, even the best ones, will at some point own investments that underperform. It is never fun and can sometimes occur when markets are highly volatile and investor sentiment is weak. As the chart below shows, there have been many such occurrences over the past decade, a relatively short period in investing history, but one with more than its fair share of major market moving events. Yet the market also shows a strong ability to recover and move higher, often quite quickly.

Market upsets, market recoveries

Value of $10,000 invested in S&P 500 over the past decade

Bloomberg, JP Morgan AM as at 30 December 2022. This hypothetical example reflects an investment tracking the returns of the S&P 500 Index. It excludes dividend reinvestments and the effects of taxes and inflation.

In time, the ‘market’ (for representative purposes we use the US S&P 500, the largest and most liquid stock market index) has shown persistence in shrugging off concerns that at the time seemed insurmountable. Remember that by selling a holding for less than they bought it for, investors will be locking in losses which are irrecoverable. They will not be able to participate in any subsequent share price recovery unless the decision is made to replace the holding with another bought at a higher level, which may adversely impact their stock and portfolio returns.

Key investment tips

Stock price volatility is normal…

And not necessarily ‘bad’. Buying when markets and stocks are in ‘sell-off’ mode can provide attractive entry points and support longer term performance when markets recover. Remember that while stocks and markets do not rise every year, the US stock market, a good example because of its size and maturity, has risen by an average 6.6% every year (accounting for inflation) since 1900.

If it was that easy...

There are many factors that influence stock pricing and sentiment, including macro factors such as geopolitics and economic conditions, as well as sector and stock changes and news flow. Regulatory changes at the supranational or national level can often exert a significant impact on investor behaviour. Remember that successful investing can be hard; if it was easy, everybody would be rich.

Invest for the long term

A long term investment is one held for a minimum of five years. Assets held to retirement could be for even longer. Historically, stock markets go up over time but this doesn’t mean all stocks will rise or outperform as a result. Diversification, or spreading wealth among different sectors and industries, can help to offset some of the unforeseen risks associated with investing in the stock market. Viewing investing as a marathon rather than a sprint will also minimise the pressure to take an emotionally driven short term decision.

Behavioural bias

Loss aversion bias is a psychological state when investors are affected more by investment losses than by the gains. This is a refinement of the ‘fight or flight’ instinct which has evolved since the dawn of mankind, when making the wrong move could have proved fatal. A loss making trade will not prove life threatening today, but in many cases an investor’s instincts will be to deal with the problem created, rather than focussing on the possibility of a recovery in the longer term.

Time in the market vs. timing the market

It shouldn’t come as a surprise, but alongside the reality that investing is hard are various studies showing that trying to time the market by staying in cash or waiting for a correction before buying can significantly underperform a ‘buy and hold’ strategy.

Generating positive returns over the longer term

Research by US broker Charles Schwab covering almost a century’s worth of US market data up to 2011 showed that a 20-year holding period never produced a negative return. More recently, Morningstar’s annual ‘Mind the Gap’ study of returns showed that investors earned a respectable 9.3% on the average dollar invested in funds over the 10 years to 2021. This was 1.7% percentage points lower than the total returns their funds generated over that period. The shortfall is accounted for by poorly timed fund purchases and sales. This effectively cost investors 17% of what they would have earned by not selling.

If you aren’t willing to own a stock for 10 years, don’t even think about owning it for 10 minutes.

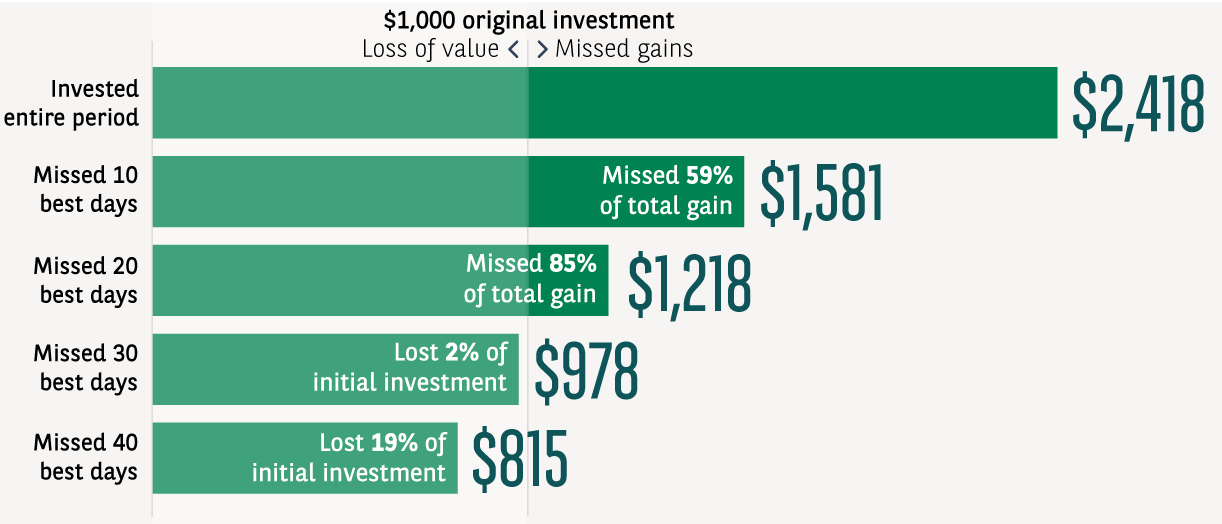

Time heals

The chart below shows the difference between investors in the MSCI All Country World Index (ACWI) who remained fully invested over the past decade and those who have not. Reinforcing the message that investors are best served by staying in the market, the chart below shows how missing out on a handful of the best return days can have a significant impact on eventual returns. Many of the best performing days occurred close to the worst and so investors selling when the prices are weak have a high chance of missing out when the market recovers.

Sources: RIMES, MSCI, as at 30 December 2022. Value of hypothetical $1,000 investment in the MSCI ACWI, excluding dividends and the effects of taxes and inflation, from 1 January 2013 to 30 December 2022

Guide to investing in volatile markets

From the importance of diversifying your portfolio to a five-point investment checklist, this guide highlights what to consider when investing in periods of market volatility.

Download guide

Find out more about navigating volatile markets

Managing market driven emotions

Volatility in global markets is normal. Despite this, and many investors' tendency towards 'loss aversion', we explain why it is important to keep to your long term goals and avoid ...

Long term investing

Stocks don't go up every year but over the long term, they have risen roughly every three years out of four in the US. We examine how higher corporate productivity and cashflow, population growth ...

Benefits of investing regularly

This is a simple and effective technique to deal with the difficulty of buying and/or selling at the right time. It encourages a disciplined approach to investing and we show ...

Behavioural biases

Behavioural biases are unconscious beliefs or thoughts that can influence our decisions, sometimes with negative consequences.

Avoiding locking in your losses

By selling a holding for less than they bought it for, investors will be locking in their losses. We examine what this means in market environments which have continued to prove resilient despite the dramatic and volatile narrative of recent years.

Buying at the dip

Market sell-offs are perhaps more frequent than you think. Despite this, the long term evidence shows that markets consistently recover. It may be daunting to consider buying after corrections, but investors should remember that these can offer opportunities for excess returns.