Long term investing

Long term investing

Markets rise and fall

It is important to recognise that stocks do not go up every calendar year and that markets move in cycles. 2022 was a punishing year for investors, while during the global financial crisis, the S&P 500 corrected 55% from its 2007 high. Yet over the long term, stocks in the US have risen roughly three out of every four years.

Inflation works its magic

Some of the rise in markets is in response to the inflationary impact on a company’s revenues and returns, as companies raise prices to offset higher raw material costs. Note though that the uncertainty associated with excessive inflation (the US Federal Reserve targets a 2% annual inflation target) has historically correlated with periods of lower equity returns.

The benefits of compounding

Compounding refers to the benefit you get by reinvesting any returns you receive on your investment. For compounding to be effective requires the reinvestment of investment returns and time.

Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.

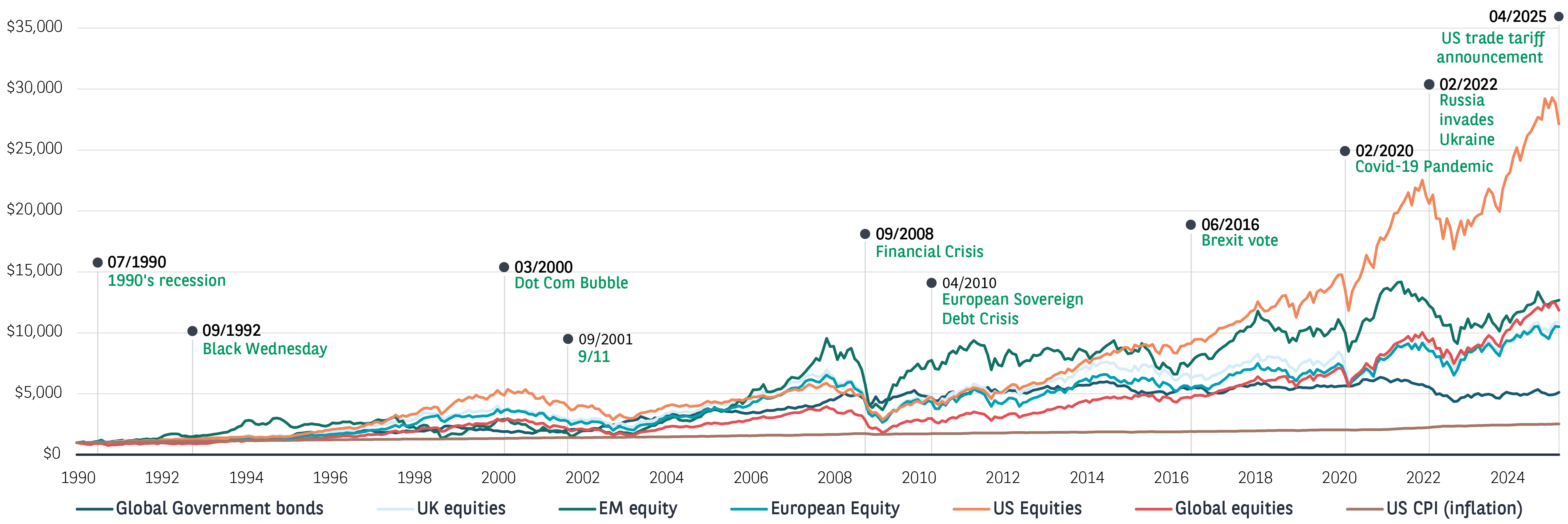

The history of long term investing

Over the years there have been many events that have had large impacts on financial markets, from black Wednesday in 1992 to the more recent financial crisis in 2008. However, as can be seen from the chart below, the long-term trend for market performance has continued to remain positive. If you are investing for the long term, while you will experience market dips and volatility from time to time, history has shown us that these events won’t stop the long-term positive performance of markets. It’s important to remember there are no guarantees though, and past performance is not a reliable guide to future performance.

Source : Morningstar, data 31 December 1989 to 31 March 2025. US dollars. Rebased to 1000. Past performance does not predict future returns.

Evolving benchmarks to represent the strongest companies

Remember that new names are entering and falling out of stock indices on a regular basis as they are ‘rebalanced’. In the case of the S&P 500, this takes place on a quarterly basis. Criteria for inclusion in the S&P 500 include a market capitalisation of at least $8.2 billion and positive earnings during the most recent quarter. The sum of its earnings over the previous four quarters must also be positive. Meeting the above requirements does not guarantee index inclusion, but the larger a company’s market capitalisation, the greater the chance of membership.

Guide to investing in volatile markets

From the importance of diversifying your portfolio to a five-point investment checklist, this guide highlights what to consider when investing in periods of market volatility.

Download guide

Find out more about navigating volatile markets

Managing market driven emotions

Volatility in global markets is normal. Despite this, and many investors' tendency towards 'loss aversion', we explain why it is important to keep to your long term goals and avoid ...

Long term investing

Stocks don't go up every year but over the long term, they have risen roughly every three years out of four in the US. We examine how higher corporate productivity and cashflow, population growth ...

Benefits of investing regularly

This is a simple and effective technique to deal with the difficulty of buying and/or selling at the right time. It encourages a disciplined approach to investing and we show ...

Behavioural biases

Behavioural biases are unconscious beliefs or thoughts that can influence our decisions, sometimes with negative consequences.

Avoiding locking in your losses

By selling a holding for less than they bought it for, investors will be locking in their losses. We examine what this means in market environments which have continued to prove resilient despite the dramatic and volatile narrative of recent years.

Buying at the dip

Market sell-offs are perhaps more frequent than you think. Despite this, the long term evidence shows that markets consistently recover. It may be daunting to consider buying after corrections, but investors should remember that these can offer opportunities for excess returns.