Close Look - Can the equity market wave continue?

What is the situation?

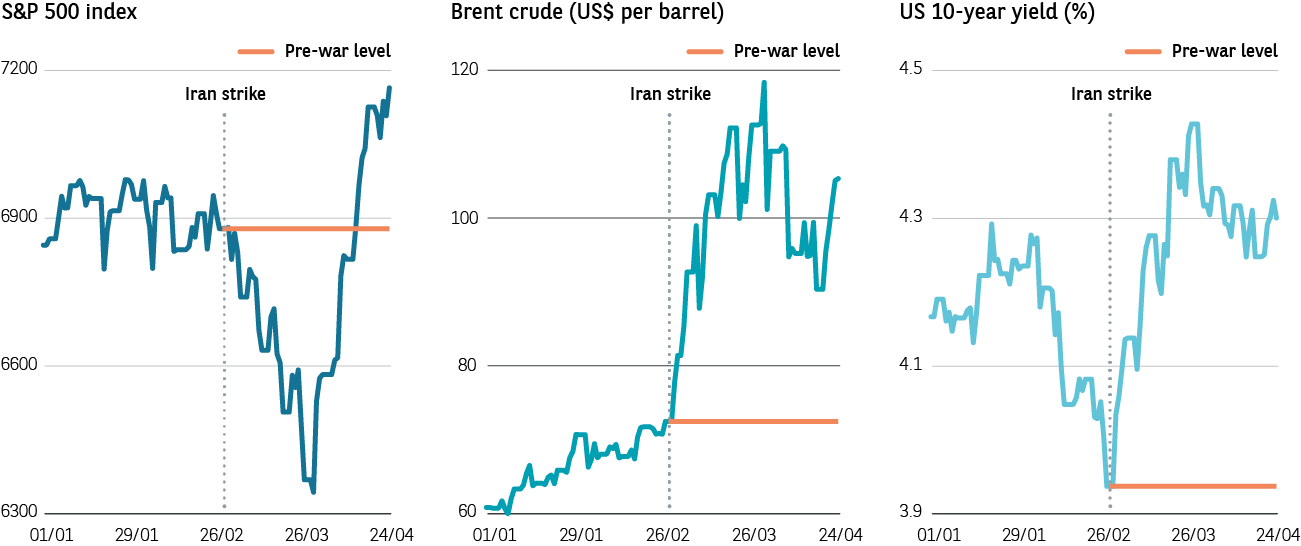

Since the announcement in early April of a temporary ceasefire in the Middle East conflict, equity markets have rallied hard. Investors grew in confidence that hostilities would gradually cease and the Strait of Hormuz would re-open, thereby allowing a fifth of global oil supply to pass freely as before. In the US, the S&P 500 index in particular embraced hopes of an early resolution and touched new record highs. Meanwhile, the performance of government bond markets diverged from equities, as seen in the chart below.

S&P 500, Brent crude price and US 10Y bond yield

Source: Bloomberg, 24 April 2026

What is the background?

US equity market performance had lagged since the peaks reached by its dominant tech sector in the autumn of 2025. In a marked rotation, emerging equity markets had been enjoying a spell of outperformance since the beginning of 2026. On the outbreak of hostilities in the Middle East, the S&P 500 fell sharply, led down by sectors such as communications and info tech. The energy sector performed strongly, however, as the price of crude oil spiked close to US$120 per barrel.

The April rally brought a sharp reversal of fortunes. Communications and info tech rebounded strongly, while the energy sector slipped back, as the price of oil traded in a range around US$100 per barrel. Meanwhile, the VIX Index of expected volatility subsided, as tensions calmed somewhat.

What about other asset classes?

Global government bond yields peaked at the end of March, then followed the US 10Y Treasury yield down, as bond prices rallied. As a reminder, bond yields move inversely to bond prices. The yield on the US 10Y Treasury remains higher than it was pre-conflict but currently appears steady at around 4.3%.

The leap in bond yields reflected fears of a resurgence in inflation, propelled by the surge in oil prices. Not surprisingly, as the chart above shows, the US 10Y Treasury yield has performed in step with the price of crude oil. Yet despite early expectations of a policy pivot from rate cuts to interest rate hikes, so far major central banks appear to have adopted a ‘wait and see’ approach. Forecasts of mid-year rate hikes have consequently been unwound.

The switch to lower US interest rate expectations has, however, impacted the US dollar, which was much in demand as a safe haven asset when the conflict broke out, but has since fallen back. Gold was hit by a significant bout of profit taking in March, although has since rallied.

Can the equity rally be sustained?

One major supporting factor is that corporate profit growth forecasts continue to be marked up, despite the geopolitical situation. Estimated average earnings growth for S&P 500 companies has jumped from 15% to 18% for the next 12 months.

These upgrades, combined with the dip in share prices, saw the market briefly trade at a valuation of less than 20 times earnings, a level last seen following the announcement of the ‘liberation day’ US trade tariffs last April. In the same way as last year, investors have stepped in to ‘buy the dip’.

Given these levels of optimism, quarterly earnings reports will be closely analysed, along with managements’ trading expectations, as the year progresses. What is more, the capital expenditure plans of the AI hyperscalers are likely to remain crucial to fuelling this positive earnings growth momentum.

Our view

The rally in US equities has been particularly sharp, but it could prove difficult to define a trend here. What is more, as the outcomes of the current geopolitical situation are still so uncertain, volatility of both economic and earnings growth forecasts is to be expected.

We believe remaining invested is the best option, although sporadic increases in cash levels are not to be ruled out. We will maintain a patient stance, seeking flexibility in an environment that should reward active management.